Risk Management to Optimize the Risk-Return Position

Content: Risk Management Resolves the Following Problems

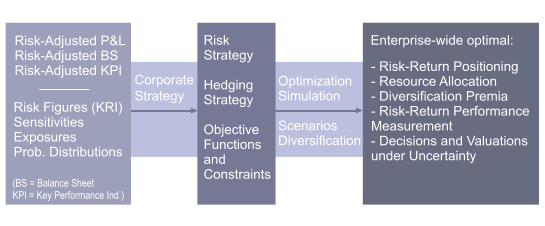

The risk management system from Noetzold & Noetzold evaluates business units, investments, projects, products, strategies, etc. under risk-return aspects, based on the results of risk controlling. The aim is a risk-adequate operational and strategic management and the development of an optimal risk strategy. Questions that will be answered by risk management are:

- What are sensible risk strategies for the company?

- What is the optimal risk strategy given the global corporate strategy?

- What is the optimal corporate risk-return positioning given the risk strategy?

- What is the optimal risk-adequate resource allocation (concerning all corporate units, subsidiaries and / or products)?

- What are the optimal investments (e.g. M&A, project, product) under risk-return aspects?

- Is the existing economic capital adequate for the current risk position or are resources wasted due to imbalance?

- What are the optimal risk limits for the corporate units?

- What is the best protection of earnings and assets against risk driver volatilities?

Objectives: Optimization of Risk-Return Positions

The objectives of risk management are:

- Development of a risk strategy consistent with the global corporate strategy.

- Efficient implementation of the risk strategy.

- Identification and optimization of the risk-return position based on risk strategy.

- Optimization of capital allocation.

- Risk-adjusted evaluation of investments and products.

- Risk-adjusted pricing.

Problems: Decision Process Without Consideration of Risk Dimension

An extensive market study Corporate Risk Management and its Integration into Operational Business sponsored by Noetzold & Noetzold identified some common problems in risk management:

- Resource allocation based on return figures (result: risk premia are not valued; risk takers are rewarded because inherent risk costs are not deducted).

- Missing portfolio optimization technology (result: unrealized corporate-wide diversification opportunities; diversification premia lost to banks, insurance companies, etc.).

- Missing risk management models (result: risk-return inefficient optimizations).

- Incorrect risk aggregation (result: incorrect consolidation of risks; incorrect risk-return figures).

- Risk aggregation with inconsistent probability distributions (result: incorrect risk figures, in particular, underestimation of extreme events, severe errors in predicting Value-at-Risk, Expected Loss, and quantiles).

- Incorrect time-dependence of risks (result: erroneous risk figures when calculating over extended periods, e.g. for projects; incorrect roll-over between periods)

- Use of standard Monte Carlo simulators (result: lack of precision/performance leading to severe errors in predicting Value-at-Risk, Expected Loss, and quantiles;

- Missing risk models (result: incorrect aggregation of risks of different type; severe errors in predicting Value-at-Risk, Expected Loss, and quantiles).

- Use of average values for risk management (result: risk average values are not risk figures, they only adjust planned values by expected or average values, they do not consider the full spectrum of all possible (not generally expected, not averaged) outcomes; risk mitigation and steering with risk average values is not risk controlling).

Solutions: Correct Risk Results Require Advanced Risk Models, Risk Aggregation, and Optimization Models

The quality of risk-return optimizations depends largely on technology, i.e. on financial/mathematical models and on a performant software implementation. Noetzold & Noetzold delivers an innovative risk management solution with the following items:

- Advanced portfolio optimization and simulation technologies.

- Correct risk aggregation (requires high-performance high-precision Monte Carlo simulator).

- Advanced risk management models (different risk types to represent risk events and market fluctuations, including interdependencies, consistent mathematical models).

- Efficient software solution (user friendly intuitive interface, compatible with corporate environment).

- Risk managers and financial engineers with extensive experience.

Results: Corporate Management under Risk-Return Aspects

The risk management is the basis for an optimal risk-adequate enterprise-wide management. The results of risk management are:

- Optimized risk-return portfolio.

- Optimal risk-return steering.

- Calculation of risk premia and risk-adjusted pricing.

- Sensitivities of risks and risk driver and their impact to earnings and cash flow.

- Future evolution of investments and products.

- Discounting to present values under uncertainty (i.e. risk-adjusted) for investments and projects.

- Risk-adjusted corporate strategy.

- Optimized risk strategy (under consideration of company's risk appetite or risk strategy).

- Risk bundles (correlated risks with large losses and preferred simultaneous occurrence).